History will record June 12, 2026 as the day Elon Musk brought his rocket company to public markets. But the instructive question for investors is what exactly they are buying at a $1.77 trillion valuation that surpasses Tesla, Meta, and Saudi Aramco's landmark 2019 debut combined.

The S-1 filing, published in late May, offered the first authoritative window into SpaceX's finances.

The picture it revealed is simultaneously more impressive and more complicated than the hype suggested.

SpaceX is, at its legacy core, a genuinely exceptional business. The satellite internet division posts operating margins that most technology companies would envy. The launch segment is deliberately loss making, ploughing capital into Starship development.

And the artificial intelligence arm, folded in through the February 2026 acquisition of xAI, lost $6.35 billion in 2025 alone. These three profiles are sold as one number. The investor's job is to decompose them.

Table of contents

- Starlink: The Engine That Funds Everything Else

- Starship and the Launch Segment: A Deliberate Deficit

- xAI and the $6.35 Billion Question

- Price to Revenue Comparison

Starlink: The Engine That Funds Everything Else

Strip away Starship ambition and xAI losses and you find a satellite internet business of striking quality.

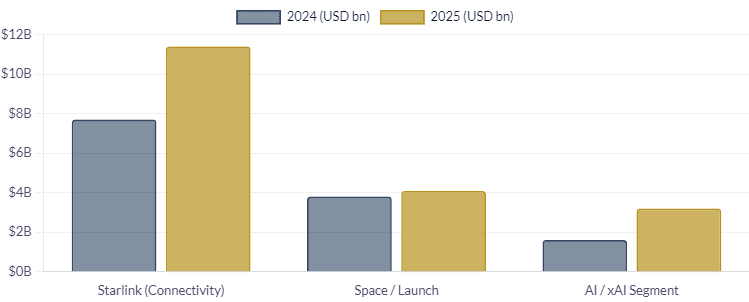

Starlink generated $11.39 billion in revenue in 2025, up 49.8% from the prior year, and produced $4.4 billion in operating income.

In the first quarter of 2026, Starlink's connectivity segment posted $3.26 billion in revenue with an operating profit of $1.19 billion, an annualised run rate approaching $5 billion in segment operating income with the subscriber base still growing rapidly.

Adjusted EBITDA for the full year reached $7.2 billion.

The subscriber count tells an equally striking story. SpaceX ended the first quarter of 2026 with 10.3 million Starlink subscribers, up from 5 million a year earlier. The doubling of the user base in twelve months, while simultaneously expanding coverage to 160 countries, suggests the penetration story retains considerable runway.

Quilty Space projects the base reaching 16.8 million by year end 2026, which would imply standalone Starlink revenue approaching $16 billion at current average revenue per user.

Starship and the Launch Segment: A Deliberate Deficit

SpaceX's space and launch business, Falcon 9, Falcon Heavy, Dragon, and Starship development, together generated $4.09 billion in revenue in 2025 while recording a $657 million operating loss.

The loss is not a sign of commercial failure; it is the output of a deliberate reinvestment cycle. The company disclosed cumulative Starship development expenditure exceeding $15 billion through 2025, above original budget projections, with a further $930 million spent on the program in the first quarter of 2026 alone.

The strategic logic is straightforward. Falcon 9 profitability at full marginal cost would be considerable, but SpaceX has chosen to redirect that surplus into Starship, which promises to reduce cost per kilogram to orbit by an order of magnitude relative to current systems.

A fully reusable heavy lift vehicle would unlock economics for the next generation Starlink V3 constellation, potential in orbit data centres, and eventually lunar and interplanetary missions. The launch segment is not a business being mismanaged; it is a capital allocation decision being made at the corporate level.

xAI and the $6.35 Billion Question

In February 2026, SpaceX acquired xAI, Elon Musk's artificial intelligence company, which itself had absorbed X (formerly Twitter) in March 2025 in an all stock transaction. Bloomberg reported the combined entity was valued at approximately $1.25 trillion at the time, placing xAI at roughly $250 billion.

That single corporate action transformed SpaceX's income statement. The AI segment, now rebranded SpaceXAI, recorded $3.2 billion in 2025 revenue alongside a $6.355 billion operating loss. In Q1 2026, the segment posted $818 million in revenue with a $2.47 billion operating loss as full quarter xAI consolidation hit the books.

The capital intensity of the AI segment is extraordinary even by the standards of the current infrastructure buildout. The Colossus data centre complex in Memphis, housing 220,000 Nvidia GPUs, built in 120 days, became the company's most capital intensive single asset in a single quarter.

The AI segment spent $7.72 billion in capital expenditure in Q1 2026 alone, against $1.33 billion in Starlink connectivity and $1.05 billion in the space segment.

Price to Revenue Comparison

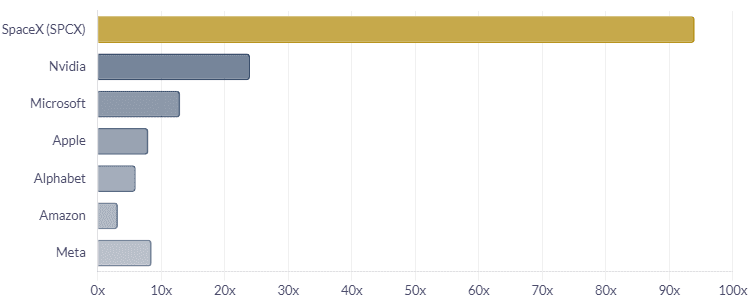

At $135 per share and 13.1 billion shares outstanding, the IPO values SpaceX at approximately $1.77 trillion, roughly 94 times its 2025 revenue of $18.67 billion.

By comparison, Amazon trades at roughly 3 times revenue and Microsoft at 13 times. Even Nvidia, whose AI infrastructure momentum commands premium multiples, trades below 25 times trailing revenue.

The SpaceX multiple is not an earnings multiple in any conventional sense; it is a bet on the size of the future markets the company is addressing.

The bull case for SPCX rests on three compounding outcomes.

Starlink continues its subscriber trajectory, reaching 20 million or more users by 2027 and sustaining average revenue per user above current levels despite emerging low Earth orbit competition from Amazon Kuiper and others.

Starship achieves commercial operational status in 2026 or 2027, unlocking satellite launch economics that slash Starlink constellation replenishment costs and open the in orbit data centre opportunity.

And xAI, despite current losses, establishes Grok as a large language model with durable enterprise distribution, benefiting from SpaceX's satellite edge compute infrastructure as a genuinely differentiated delivery mechanism.

The bear case is less a single scenario than a sequencing problem.

Starlink's revenue per user is already showing signs of compression as the company pursues volume via lower tier pricing.

xAI's $7.72 billion quarterly capital expenditure rate, if sustained, would consume Starlink's operating profits entirely.

Starship delays beyond 2027 would extend the launch segment's loss period while deferring the satellite cost improvement that the entire constellation economics depend upon.

And any perceived change in Musk's attention, across Tesla, xAI, X, and now SPCX, triggers the multiple compression that a 94 times revenue valuation cannot absorb without severe share price consequences.