Something remarkable happened during the Q1 2026 earnings season. The four largest technology companies in the world, Amazon, Alphabet, Microsoft, and Meta, disclosed combined capital expenditure plans totalling $725 billion for the year.

That number is not a rounding error. Two years ago, in 2024, the same group spent just over $200 billion combined. By 2027, Wall Street estimates have already crossed the $1 trillion mark.

This is not an incremental investment. It is a structural reshaping of the global technology industry, where compute infrastructure has become both the primary competitive moat and the defining battlefield.

For investors, the questions that matter are not whether this spending is large. They are: what is it buying, can the revenue justify it, what does it do to free cash flow and balance sheets, and what are the investable implications?

This piece works through each of those questions in turn, anchored in the most recent earnings disclosures, analyst projections, and independent research available as of May 2026.

Table of contents

- How Much Are They Spending?

- What Is It Doing to Free Cash Flow?

- Dependence on Future Earnings

- Closing View

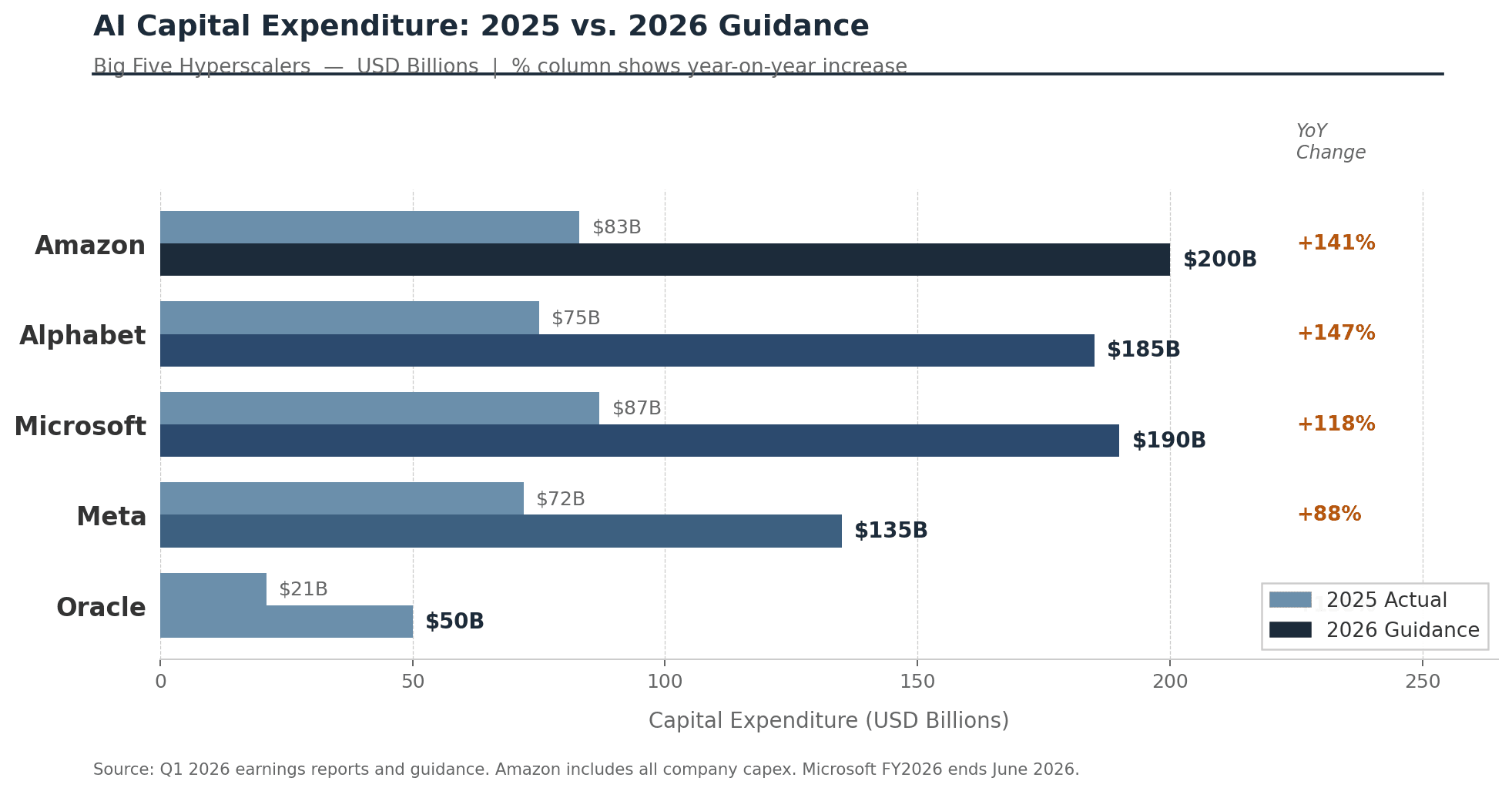

How Much Are They Spending?

The numbers require a historical anchor to appreciate. In 2022, the five largest hyperscalers; Amazon, Alphabet, Microsoft, Meta, and Oracle collectively spent $162 billion on capital expenditure.

By 2025, that figure had reached $448 billion. In a single quarter, Q4 2025, these five companies deployed a combined $140 billion, more than their entire annual budget of a few years prior. Epoch AI estimates the group has grown capex at an average annual rate of 72% since Q2 2023.

The acceleration is not confined to the US.

In January 2026, the Stargate consortium, comprising OpenAI, SoftBank, and Oracle committed to a $500 billion infrastructure programme over four years.

Chinese hyperscalers Alibaba, ByteDance, and Tencent are simultaneously scaling their own AI infrastructure, as are Middle Eastern sovereign funds deploying multi-billion-dollar data centre investments.

Goldman Sachs projects cumulative hyperscaler capex of $1.15 trillion across 2025 to 2027, which is nearly three times the $477 billion spent from 2022 to 2024. McKinsey estimates cumulative global AI infrastructure investment could reach $6.7 trillion by 2030.

Roughly 75% of the Big Five's 2026 spending is directly attributable to AI infrastructure, GPU clusters, data centre construction, networking, and AI-optimised storage, rather than traditional cloud or logistics capex. Hyperscalers are now spending between 45% and 57% of revenue on capital expenditure. That ratio previously belonged to utilities and industrial companies. Technology firms were never supposed to look like this.

What Is It Doing to Free Cash Flow?

Free cash flow is the number that ultimately drives valuation. It is what remains after a company funds its operations, pays taxes, and spends on capital investment.

It is the money that can return to shareholders or fund further growth. When capex doubles or triples in two years, free cash flow does not just compress. In some cases, it disappears.

The four largest hyperscalers generated a combined $200 billion in free cash flow in 2025, down from $237 billion in 2024, despite strong operating performance. In 2026, with capex plans running well ahead of operating cash flow at several companies, the trajectory gets significantly worse.

| Company | 2026E Capex | FCF 2025 | FCF 2026E | Cloud Backlog |

|---|---|---|---|---|

| Alphabet | $180-190B | $73.3B | ~$8B | $462B (+100% QoQ) |

| Amazon | $200B | $38B | Negative | $460B+ |

| Microsoft | $190B | $74B | ~$53B | $315B |

| Meta | $125-145B | $52B | ~$20-30B | N/A |

Dependence on Future Earnings: How Real Is the Revenue Gap?

The structural question is direct: these companies are making multi-year, largely irreversible capital commitments today based on revenue trajectories that do not yet exist at the necessary scale.

That is not inherently irrational, all infrastructure investing works this way. But the speed and magnitude of this cycle create forward dependencies that investors need to understand explicitly.

The $2 Trillion Revenue Target

Bain Capital estimates that the hyperscaler data centres being constructed today will need to generate $2 trillion in annual revenue by 2030 to justify their cost. The current annual run rate of cloud and AI-related revenues across the ecosystem is approximately $300 to $400 billion.

Bridging that gap requires AI to move from enterprise experimentation to an embedded productivity layer across healthcare, financial services, manufacturing, logistics, and professional services, within four to five years, and to monetise at the scale those industries demand.

Customer Concentration Risk

A less-discussed dimension is customer concentration within the AI supply chain. OpenAI and Anthropic are two of the largest consumers of hyperscaler AI infrastructure in 2026.

Both are pre-profit, venture-backed companies whose ability to continue absorbing infrastructure costs depends on continued capital raising and eventual revenue scaling of their own. If AI application companies, which anchor a meaningful slice of current hyperscaler demand, cannot monetise their products as projected, hyperscalers face both revenue shortfalls and potential asset utilisation problems on committed infrastructure.

The Hardware Upgrade Treadmill

GPU architectures are not static assets. The hardware required to run 2026's most demanding AI workloads will differ materially from what is needed in 2028. Each new model generation demands faster interconnects, higher memory bandwidth, and greater power density.

This creates a treadmill dynamic: companies that pause capex risk falling behind on capacity, but companies that continue face the possibility that installed assets are obsoleted before they are fully depreciated.

Infrastructure built today on 2025 assumptions must serve workloads whose performance requirements are still being defined.

Closing View

The most instructive historical parallel for the current AI capex cycle is probably the buildout of fibre optic infrastructure in the late 1990s.

That infrastructure was genuinely necessary and transformative. The internet did become as important as its proponents claimed. But the pace of monetisation was far slower than the capital committed assumed.

Many of the companies that deployed that capital did not survive to see the returns. The infrastructure they built was ultimately used, but by different companies, at different price points, than the original investment thesis required.

The hyperscalers today are not 1990s telecoms startups. They have balance sheets, diversified revenues, and contracted demand that those companies lacked. The probability of permanent capital loss is lower.

But the question of whether free cash flow recovers on the timeline implied by current valuations is not settled. The market has already made preliminary judgements, rewarding Alphabet and Amazon where cloud revenue provides visible ROI, penalising Meta where it does not. Those judgements will continue to be refined as 2026 and 2027 earnings reveal how closely the revenue trajectory tracks the capex commitment.

For investors, the investable insight is not the aggregate capex number. It is the discipline to distinguish between companies where today's capital expenditure is converting into tomorrow's contracted revenue, and those where it remains, for now, an act of faith in a future that has not yet arrived.